What Are the Different Card Fraud Types and How Can They Be Prevented?

From AI-driven synthetic identities to account takeovers and skimming, each fraud type has its own behavioral signature. A one-size-fits-all approach doesn't work.

For financial services practitioners, risk managers, and fraud detection specialists, card fraud presents a challenge that continues to evolve. Understanding card fraud requires an examination of the entire fraud lifecycle, from the initial compromise of Personally Identifiable Information (PII) to the reselling of stolen credentials, to the detection logic required to stop fraudulent transactions without disrupting the legitimate ones.

Key Takeaways

- Card fraud operates as an organized supply chain. Modern fraud is not a single criminal act but a structured ecosystem involving data harvesters, dark web marketplaces, and "cashers" who convert stolen information into profit. Understanding this lifecycle is essential for building effective defenses at each stage.

- Fraud types are diverse and require distinct detection strategies. From AI-driven synthetic identities to account takeovers and skimming, each fraud type has its own behavioral signature. A one-size-fits-all approach to fraud detection will leave institutions exposed to the types it wasn't designed for.

- Effective fraud prevention balances risk mitigation and customer experience. Detection systems must minimize fraud losses without disrupting legitimate transactions. Tools like machine learning models and real-time two-way customer communication all play a role in striking that balance.

- Speed and data integration are the foundation of fraud response. Whether flagging a suspicious transaction, issuing provisional credit, or gathering evidence during an investigation, the entire fraud lifecycle depends on connecting signals across disparate systems quickly. Isolated data points often look benign; combined in real time, they can reveal fraud patterns that would otherwise go undetected.

The Anatomy of Modern Card Fraud

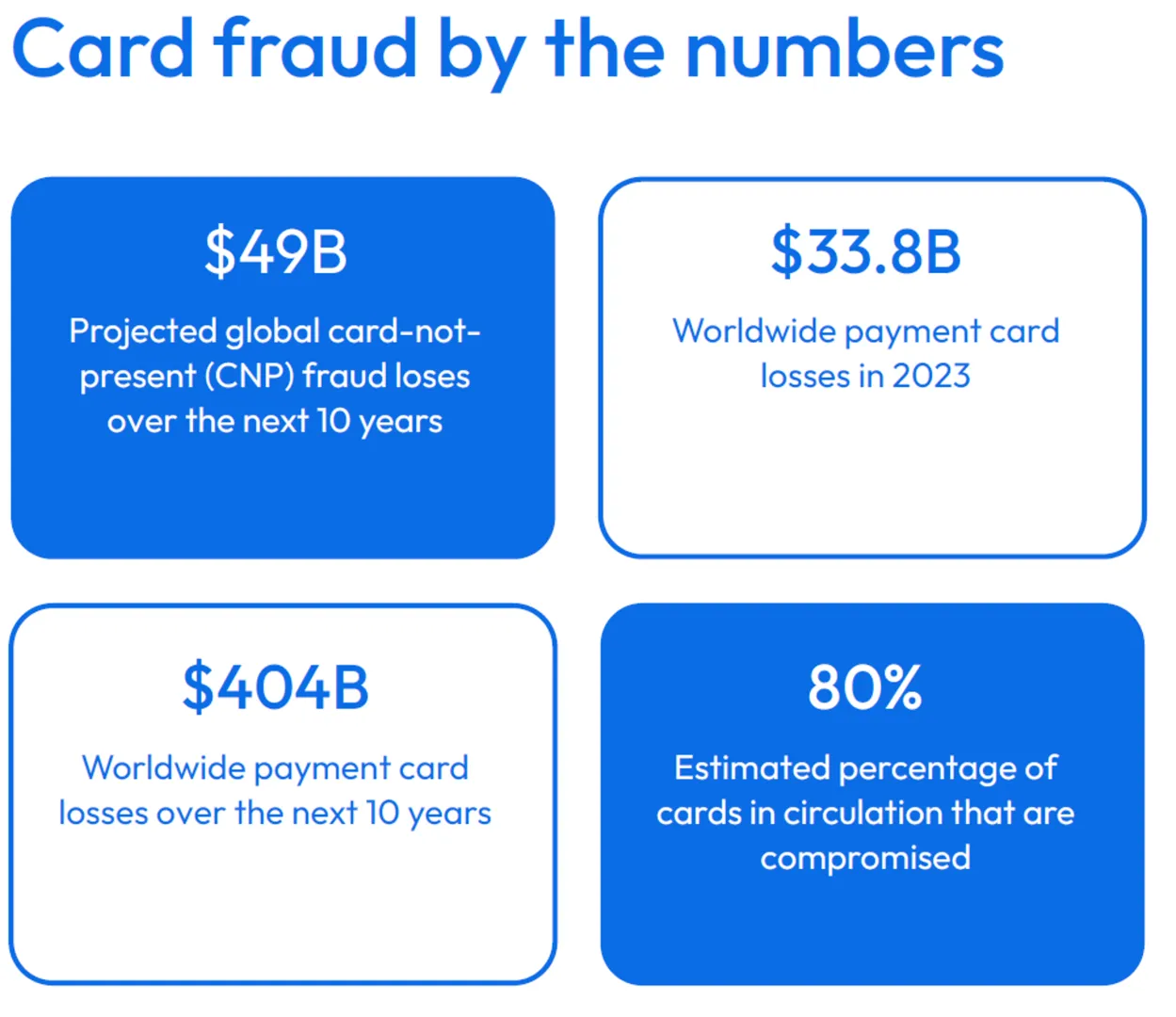

At its core, card fraud involves the unauthorized use of a credit or debit card, or the card number (PAN), to fraudulently obtain money or property. The ecosystem of credit card fraud functions much like a legitimate supply chain. "Producers" harvest data through breaches or skimming. "Wholesalers" aggregate and validate this data on the dark web, selling "dumps" (magnetic stripe data) or "fullz" (full identity packages). “Cashers” turn stolen data into profit by buying goods for resale or using money mules.

Source: Hot Topic Q&A – Tackling Card Fraud in an Era of New Technology | FICO

What Are the Main Types of Card Fraud

To effectively detect and prevent fraud, practitioners must categorize attacks into specific type. Each type presents unique behavioral signatures and requires distinct mitigation strategies.

AI Fraud

With the rise of AI and particularly deepfakes, 26% of financial institutions recently surveyed reported increases in fraud attempts of 51% or higher in the past two years. AI has lowered the barrier to entry for fraudsters, making it easier to create synthetic identities, use deepfakes to take over accounts, and plan AI-driven bot attacks.

Source: Fraud in the Age of AI: Trends, Threats, and Management Tactics

Card-Not-Present (CNP) Fraud

Following the global adoption of EMV (Europay, Mastercard, and Visa) chip technology, which significantly secured physical Point of Sale (POS) transactions, fraud migrated aggressively to online channels. Card-Not-Present (CNP) fraud occurs when a criminal uses stolen card details to make a purchase via phone or internet without the physical card being involved.

CNP fraud is difficult to detect due to the volume and speed of transactions. Fraudsters use automated scripts in "carding" or "BIN attacks" to test stolen card numbers, often with small transactions from different locations, followed by larger purchases once the card has been validated.

Account Takeover Fraud

Account Takeover (ATO) fraud is a broad category of fraud, largely associated with identity theft, which can impact card account holders as well as other kinds of accounts (e.g., checking/savings, investment, loan, social media, etc.).

Rather than simply using a stolen card number, the fraudster gains access to the cardholder's legitimate account management portal. This can be achieved through credential stuffing (using username/password pairs stolen from other breaches), targeted phishing attacks, social engineering, and other manipulative tactics.

Fraudsters accessing accounts can change associated passwords, phone numbers, email accounts, and shipping addresses. They can also request cards be delivered to drop sites, or add themselves as authorized users to the account.

Account takeover is hard to detect, as transactions often use valid credentials. Detection and monitoring of non-monetary signals like PII changes, password resets, and risky device or IP logins, as well as out-of-pattern transactions, can help identify ATO fraud.

Triangulation Fraud

Triangulation fraud involves a three-party deception. A fraudster sets up a fake online storefront offering high-demand goods at steep discounts. A customer buys an item, providing their card data to the fraudster. The fraudster then uses stolen card data from a different consumer to buy the item from a legitimate merchant, which ships it to the customer.

The customer receives their item and is satisfied. The fraudster keeps the customer’s payment and can use it to commit future fraud. If the consumer whose card was stolen complains, there may be a further loss for the merchant in the form of a chargeback.

Physical and Digital Skimming

Skimming remains a persistent threat for both debit and credit cards. In the physical world, fraudsters attach "overlays" to point-of-sale (POS) machines, ATM card slots, and gas pump terminals. These devices read the magnetic stripe data while a hidden camera or pin-pad overlay captures the PIN. This allows for the creation of cloned cards, which can then be used for purchases or cash withdrawals.

Formjacking, or Magecart attacks, are the digital equivalent of physical card skimming and occur when criminals inject malicious JavaScript into checkout pages to secretly capture and steal customers’ payment information during transactions on trusted websites.

Phishing and Social Engineering

Phishing uses fake emails, texts (smishing), or calls (vishing) posing as trusted sources to create urgency and trick victims into giving up personal information and login details for accounts, or scam customers into paying fictitious fees (e.g., parcel delivery charges).

A common variation involves the "fraud department" scam. A criminal calls the victim, claiming to be the bank's fraud team, stopping a suspicious charge. They ask the victim for the code sent to their phone "to verify identity." In reality, the criminal is attempting an account takeover using compromised credentials and has triggered a password reset or a transaction, and the code sent to the legitimate consumer is the two-factor authentication token needed to complete the theft.

Data Breaches and Stolen Card Data

When major data breaches occur, the stolen card information enters a shadowy underground economy known as the dark web. The stolen data is sold on the dark web and the criminals who purchase it then attempt to use the cards for fraudulent purchases. This creates a time-sensitive criminal economy where speed is essential, and it explains why fraud alerts and account monitoring have become so crucial for protecting consumers.

The Detection and Prevention Methods Used to Combat Card Fraud

Prevention is about establishing a system that finds a balance between risk mitigation and customer experience. A system that blocks 100% of fraud but declines 20% of legitimate transactions is operationally untenable.

Advanced Analytics and Machine Learning

Institutions rely on sophisticated supervised and unsupervised machine learning models to help identify and intervene when fraud is suspected. Fraud analytics can leverage both of these advanced techniques to spot risk and predict fraud accurately for fast, informed decisions.

- Supervised learning uses tagged historical data (where known fraud vs known legitimate transactions are clearly identified) to identify patterns indicative of fraud vs non-fraud. These models then score each transaction in milliseconds by analyzing complex combinations of data like address, IP, and timing.

- Unsupervised learning analyzes unlabeled transaction data to detect anomalies, such as unexpected behavior or new, unknown fraud types.

FICO's applied analytics and machine learning capabilities are foundational to independent fraud detection and advanced risk management. FICO® Platform leverages machine learning and real-time analytics to detect evolving fraud tactics and adapt its fraud detection responses. It supports regulatory compliance, ensures model transparency, and enables scalable analytics.

3D Secure and Multi-Factor Authentication (MFA)

3D Secure (e.g., Verified by Visa, Mastercard Identity Check) adds authentication for online payments. With 3DS 2.0, low-risk transactions are approved automatically after issuer assessment, while high-risk ones require biometric or OTP verification.

Integrating Transactional Data Across Silos

A critical best practice for fraud managers is the integration of data across silos. Fraud signals often exist in disparate systems and from different sources: the call center logs, the online banking portal, the bank’s host system, the ISO message for the authorization, the fraud prevention system itself, and often data from third-party providers or risk models. By integrating these data sources, a bank can see that a customer just called to change an address (call center data) immediately before a high-value purchase was attempted (transaction data). Isolated, these events look benign; combined, they can indicate an account takeover.

Real-Time Customer Communications

When fraud is suspected, instant verification makes the difference between a good customer experience and outcome and one that results in financial and reputational losses. Banks increasingly rely on two-way, omni-channel communications to contact the customer using their preferred channel. Using such communications, they can take actions such as sending an SMS to break the scammer’s spell, sending an alert in the bank app to help stop a push payment, or send the customer a self-resolution option where they can confirm or deny that a transaction is fraudulent. Furthermore, customers have come to expect an elevated customer experience when communicating with their bank, making omni-channel communications a “must have” rather than a “nice to have” when it comes to proactive fraud prevention and ongoing fraud management.

What Happens When Card Fraud Is Detected

When fraud is suspected or reported, a standardized operational workflow is triggered. This process is critical for regulatory compliance and loss mitigation.

Detection, Alerting and Investigation

The cycle begins when the fraud engine flags a transaction. Based on available risk scores and a range of conditions, the system may make authorization and case creation decisions in alignment with the bank’s fraud policy and risk appetite. How these alerts (cases) are then treated varies according to risk, fraud methodology, customer segment, and workflow options available (e.g., automated case working, automation with human in the loop, versus a fully manual approach).

Resolution and Recovery

If the investigation confirms fraud, the bank will attempt recovery through the chargeback process if merchant liability applies. Merchant liability is often determined by the security measures which were in place at the time the transaction was made; for example, if a merchant requires 3D-secure verification or other secondary verification at the time of purchase, then the merchant is not liable for the loss. Banks will typically be able to recover unsecure losses.

If the investigation proves the customer did authorize the charge (or benefited from it), the case will instead be treated as first-party fraud, and the customer will be treated according to the bank’s policy.

FICO's Commitment to Card Fraud Prevention

FICO has been a proven leader in card fraud detection and prevention for more than three decades. We offer out-of-the-box card fraud consortium models that deliver immediate value to businesses across the world. Our FICO® Falcon® Intelligence Network provides insights from billions of tagged transactions every year from more than 10,000 participating global financial institutions, giving all our fraud customers unparalleled performance.

FICO’s consortium models are one tier in a multi-layered defense strategy. FICO also provides innovative and industry-leading capabilities through Enterprise Fraud Solution powered by FICO Platform, and FICO® Falcon® Fraud Manager, to allow for the end-to-end orchestration of fraud management from detection through to investigation. Whether fighting card fraud, application fraud, scams, or other criminal activities, FICO offers a comprehensive approach that allows enterprises to deliver seamless, consistent protection across products, portfolios, and channels.

FICO's continuous, proven fraud-fighting innovation, powered by artificial intelligence and machine learning has been recognized for the sixth time in a row by Chartis’ Enterprise and Payment Fraud Solutions 2026, Quadrant Update. FICO has been named a category leader in three categories: enterprise fraud solutions, payment fraud solutions and fraud platforms.

How FICO Supports and Strengthen Enterprise Fraud Management

- Learn how FICO® Falcon® Fraud Manager has helped UBS Card Center decrease card fraud by 74%

- Read our white paper on scams and mules in Southeast Asia and access a 5-year roadmap to building a defensible framework

- Download the Beyond Point Solutions: Orchestrating the Future of Fraud Prevention analyst report to better understand the fraud orchestration market

- Explore FICO’s card fraud solutions and how they help detect and prevent global card fraud

- Learn more about the impact of the rise on card fraud attacks and how FICO is successfully helping fraud fighters combat card fraud in this Q&A with FICO’s fraud prevention expert Neil Mason

Frequently Asked Questions

Large financial institutions benefit from vast transaction datasets that improve the accuracy of their machine learning models over time. Smaller banks and credit unions may not have the same data volume, but they are not without options. Consortium data networks, like the FICO® Falcon® Intelligence Network, allow smaller institutions to benefit from fraud signals aggregated across thousands of participating organizations globally. Smaller institutions can also directly access FICO’s enterprise-level fraud detection and intervention technology through a global network of processor and partner organizations.

Striking the right balance between fraud prevention and customer experience is one of the central operational challenges for fraud managers. In practice, institutions use a combination of risk scoring thresholds, segmentation strategies, and champion-challenger model testing to tune their systems over time. Key metrics like false positive rates, fraud escape rates, and customer friction scores are tracked continuously. Responsibility for managing this tradeoff typically spans fraud operations, data science, and customer experience teams working in close alignment.

Traditional model retraining cycles can take weeks or months, which creates a window of exposure when entirely new fraud tactics emerge. Leading fraud platforms address this by combining supervised models, which are updated periodically with new labeled data, with unsupervised anomaly detection that can flag unusual patterns in real time without waiting for a model refresh. The speed at which an institution can identify, label, and incorporate new fraud patterns into its models is increasingly a core competitive differentiator in fraud management.

Liability in card fraud is not fixed and depends on several factors, including the payment channel, the authentication methods used, and the specific rules of the card network involved. Generally speaking, when EMV chip technology is available but a merchant processes a transaction using a magnetic stripe instead, liability shifts to the merchant. In CNP transactions, liability rules vary by network and region, and the adoption of 3D Secure authentication can shift liability away from the merchant when it is properly implemented. For fraud managers and merchants alike, understanding where liability sits is a meaningful incentive to invest in stronger authentication and fraud controls.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

Average U.S. FICO Score at 717 as More Consumers Face Financial Headwinds

Outlier or Start of a New Credit Score Trend?

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.